Amid concerns of rising interest rates and surge in dollar index coupled with widening current account deficit, the rupee fell to its lowest ever level of nearly 82.00 against the US greenback. The rupee has depreciated by more than 10% against the dollar so far this year to hit record low despite frequent interventions by the central bank. India’s ballooning trade gap and capital outflows are raising new risks for the rupee, just as the currency’s plunge to a record low adds to inflation woes. Indian rupee is expected to remain under pressure due to the faster pace of interest rate hikes by the US Federal Reserve.

Indian Rupee at life time low

Overview

Amid concerns of rising interest rates and surge in dollar index coupled with widening current account deficit, the rupee fell to its lowest ever level of nearly 82.00 against the US greenback. The rupee has depreciated by more than 10% against the dollar so far this year to hit record low despite frequent interventions by the central bank. India’s ballooning trade gap and capital outflows are raising new risks for the rupee, just as the currency’s plunge to a record low adds to inflation woes. Indian rupee is expected to remain under pressure due to the faster pace of interest rate hikes by the US Federal Reserve. Volatile oil prices are also expected to take a toll on the currency.

The Reserve Bank of India (RBI) may increase the repo rate up to 50 basis points in its policy statement on September 30. RBI has already increased the repo rate three times since May. During this period the key policy rate has risen from 4 per cent to 5.40 per cent. If RBI increases rates by 50 bps in this monetary policy then the repo rate may reach 5.90 per cent.

In near to medium term USDINR is expected to depreciate further amid rising inflationary pressure and surge in interest rates, stronger dollar index and rising current account deficit. It is expected to move towards 83-83.5 in medium term while taking support near 80-80.5 levels.

Factors affecting USDINR

Fed hike interest rates

Recently US Federal Reserve (Fed) raised its benchmark interest rate by 75 basis points in its Sep meeting to tame the 40-year high inflation. US Federal Reserve increased the federal funds rate, its key short term interest rate, by 75 basis points to 3-3.25%.US central bank remains stubbornly aggressive and hawkish, indicating more rate hikes are likely before the end of this year. The Fed is now raising rates at one of the fastest paces in its modern history. By 2023, the Fed could raise rates to as high as 4.5 percent, according to the US central bank’s announced plan. The Fed predicts the US economy will crawl along at 0.2 percent this year. And in 2023 it seems that the US economy can hardly escape recession.

Global Rise in Inflation

Rising inflation globally is prompting various central banks to raise interest rates which will result in slowing economic growth. US Fed is determined to quash elevated inflation that is seeping through the country’s economy, with the most recent data showing inflation remaining stubbornly elevated at 8.3 percent in August, 2022 with large price rises in shelter, food, health care and education. Rising inflation across the globe is a cause of concern including in India as price hike over time reduces the purchasing power of consumer. India retail inflation moved higher to 7 per cent in August 2022 due to higher food prices. The figure stood at 6.71 per cent in July 2022.

Dollar index…Near 20 year highs

Dollar index jumped to its highest since May 2002 at 114.5 recently, majorly due to the weakness in the euro, which hovered close to a 20-year low near parity to the dollar amid concerns that an energy crisis could tip Europe into recession, while the U.S. Federal Reserve continues to aggressively tighten policy to curb inflation. So the broad rally in greenback have resulted in weakness in major currencies is across the world like euro, British pound and including Indian rupee.

Rise in US treasury yields

The U.S. 10-year Treasury yield was approaching 4%, breaching levels not seen since 2010, sparked by elevated expectations for Federal Reserve interest-rate increases and stickier inflation. The yield — used as a benchmark for borrowing costs in the real economy has scaled from 1.5% in January 2022.

Rising CAD (Current account deficit)

India’s current account deficit (CAD), a key indicator of balance of payment of a country, is likely to remain within 3 per cent of the GDP in 2022-23 as against 1.2 per cent during the last fiscal, according to an article published in the Reserve Bank’s bulletin. The widening trade deficit, or the gap between the value of imports and exports, puts pressure on the balance of payments. India’s trade deficit during the first five months of 2022-23 widened to USD 124.5 billion from USD 54 billion in the previous corresponding period.

Monthly Chart of DOLLAR INDEX

Analysis

Dollar index have witnessed sharp upside movement on Monthly charts as it moving above 10, 20 and 50 day moving averages. RSI on daily charts is above 80 indicating that it is in overbought zone. On monthly charts it has key resistance near 120 levels .Overall it can move in range of 110-120 in next couple of months.

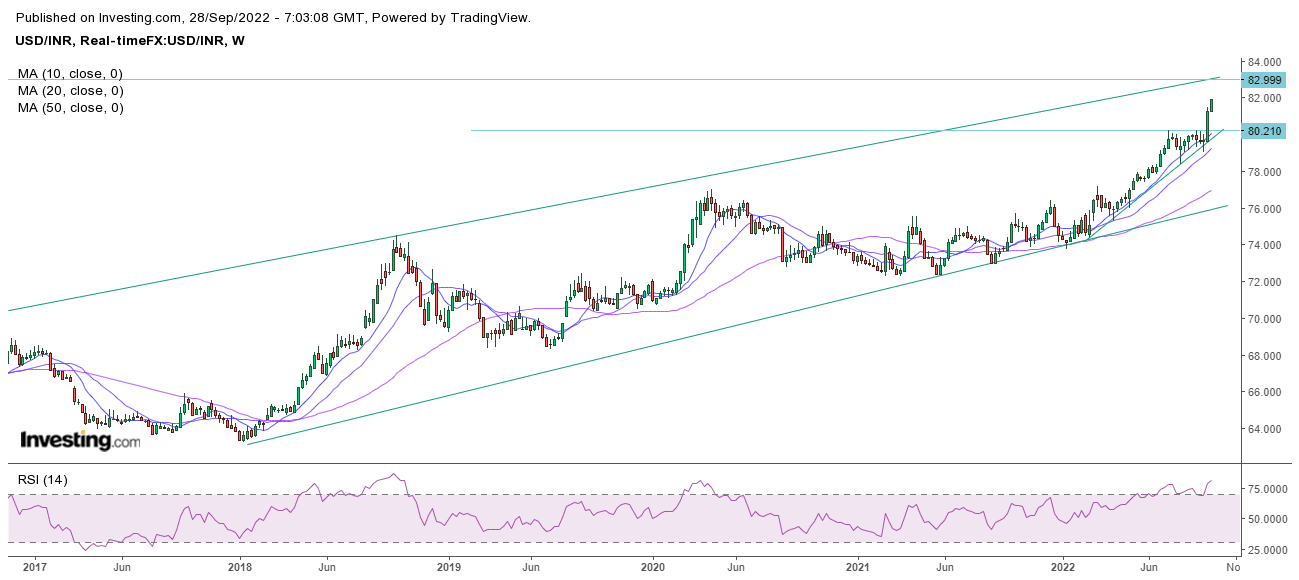

Weekly Chart of USDINR FUTURES SPOT

Analysis

Weekly chart of USDINR spot is showing steady upside movement as it is moving above the 10, 20 and 50 day moving average. RSI indicator have moved above 80 thus indicating that prices are overbought. USDINR has recently broken the key resistance of 80.3 and now heading towards upside channel resistance of 83 levels.

Disclosure

Globe Capital Market Limited (“GCML”) is a Stock Broker registered with BSE, NSE, USE and MSEI in all the major segments viz. Capital, F & O and CDS segments. GCML is also a Depository Participant and registered with both the Depositories viz. CDSL and NSDL. Further, GCML is a SEBI registered Portfolio Manager. GCML includes subsidiaries, group and associate companies, promoters, directors, employees and affiliates.

Globe Commodities Limited, Globe Derivatives and Securities Limited & Globe Fincap Limited are subsidiaries of GCML. Rolex Finvest Private Limited, A to Z Consultants Private Limited, A to Z Venture Capital Limited, M. Agarwal Stock Brokers Private Limited, A M Share Brokers Private Limited, Shri Adinath Advertising Company Pvt. Ltd., Orient Landbase Private Limited, Bolt Synthetic Private Limited, Price ponder Private Limited and Lakshya Impex Private Limited are associates of GCML. Globe Comex International DMCC is step down subsidiary of GCML.

This report has been prepared by GCML and published in accordance with the provisions of Regulation 19 of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for general circulation or public distribution. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available to others, in any form, in whole or in part, for any purpose without prior written permission from GCML. The projections and the forecasts described in this report are based on estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections are forecasts were based may not materialize or may vary significantly from actual results and such variations will likely increase over the period of time. This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into account the particular investment objective, financial situation or needs of any individual in particular. The research analysts of GCML have adhered to the code of conduct under Regulation 24 (2) of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their own investment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particular circumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. GCML does not take any responsibility thereof.

Any such recipient shall be responsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved in securities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investors may realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.

This report has been prepared by GCML based on the information available in the public domain and other public sources believed to be reliable. Though utmost care has been taken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by GCML that such information is accurate or complete and/or is independently verified. The contents of this report represent the assumptions and projections of GCML and GCML does not guarantee the accuracy or reliability of any projection, assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable or appropriate to recipients’ specific circumstances.

Since GCML or its associates are engaged in various financial activities, they might have financial interest or beneficial ownership in various companies including subject company/companies mentioned in the report. GCML or its associates have not received any compensation for investment banking or merchant banking from the subject company in the past 12 months. GCML or its associates might have received any compensation including brokerage services and for products or services other than investment banking or merchant banking from the subject company in the past 12 months. It is confirmed that GCML or research analyst or its associates have not managed or co-managed public offering of securities for the subject company in the past 12 months.

Research analyst or GCML or its relatives’/associates’ have no material conflict of interest at the time of publication of this report. Neither research analyst nor GCML are engaged in market making activity for the subject company. It is confirmed that research analysts do not serve as an officer, director or employee of the subject company. It is also confirmed that research analyst have not received any compensation from the subject company in the past 12 months.

No material disciplinary action has been taken on GCML by any regulatory authority impacting Equity Research Analysis activities.

The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. This information is subject to change, as per applicable law, without any prior notice. GCML reserves the right to make modifications and alternations to this statement, as may be required, from time to time.

Research analyst or GCML or its relatives’/associates’ do not have actual/beneficial ownership of 1% or more in securities of the subject company, at the end of the month immediately preceding the date of publication of the document.