White metal silver has witnessed roller coaster ride as decline in greenback and increase in industrial demand to assisted its prices. Overall its prices can take support near 68000 -69000 and can face resistance near 78500-79000 in near to medium term.

Overview and Outlook

White metal silver has witnessed roller coaster ride as it rose swiftly higher in beginning of October from nearly 66000 to above 77800 in last week of November 2023 aided by decline in greenback and increase in industrial demand .But in first week of December prices witnessed sharp pullback towards 72000 thereafter stabilizing near 74000 levels. Meanwhile expectations that the Fed will start cutting rates, along with the expectation of a weaker US dollar should see investment demand return, following strong ETF outflows in near term. Stronger investment demand, combined with a continuation of central bank buying can be bullish for silver prices. Silver Industrial demand is expected to grow 8% to a record 632 million ounces (Moz) in 2023. Key drivers behind this performance include investment in photovoltaics, power grid and 5G networks, growth in consumer electronics, and rising vehicle output. Overall its prices can take support near 68000 -69000 and can face resistance near 78500-79000 in near to medium term.

Factors impacting Silver prices

Movement in Dollar index:

The dollar index has seen sharp fall in past two months as it fell from 106.98 to below 102 thereby assisting silver prices. The anticipation of rate cuts by the Federal Reserve, highlighted by the market’s expectation of easing as soon as March, places downward pressure on the dollar. Additionally, the dovish stance of other major central banks, including the ECB and the Bank of England, further contributes to this sentiment. In medium term dollar index can move in range of 99-105.

Key highlights of recent Fed meeting

The US Federal Reserve opted to maintain its key interest rate for the third consecutive time on December 13, laying the groundwork for anticipated multiple cuts in 2024 and beyond. The Fed’s policymakers also signaled that they expect to make three quarter-point cuts to their benchmark interest rate next year, fewer than the five envisioned by financial markets and some economists. The relatively few numbers of rate cuts forecast for 2024, which may not begin until the second half of the year suggest that the officials think high borrowing rates will still be needed for most of next year to further slow spending and inflation.

Global total silver demand

Globally, total silver demandis forecast to ease by 10% to reach 1.14 billion ounces in 2023. Gains in industrial applications will be offset by losses in all other key segments. Silver jewelry and silverware demand is set to fall by 22% and 47%, respectively, to 182 Moz and 39 Moz this year. For both, losses are led by India, where full-year demand is expected to normalize after a surge in 2022. Excluding India, global jewelry demand is expected to edge slightly higher in 2023, while silverware will fall by a notably smaller 12%.

Surge in industrial demand of silver

The boost in silver largely comes from the industrial demand, especially from China. Though both gold and silver are considered safe-haven assets, silver is more of an industrial metal recently. Almost 60 per cent of global consumption of silver is accounted for industrial usage and the rest is for investment purposes. Silver has been a valuable commodity for centuries, prized for its beauty, durability, and versatility. It has been used in coins, jewellery, and various industrial applications such as electronics, medicine, and photography. However, in recent years, new demand areas for silver have emerged driven by advances in technology and changes in consumer behavior. Silver is currently largely used in the areas of renewable energy such as solar and wind power. As per Silver Institute data, silver demand from the photovoltaic sector climbed 15 percent last year and is likely to surge 28 percent this year. Silver demand from this sector has been three times higher than its 2015 levels.

Demand from Electric vehicles

In past few years there has been increase in usage of electric vehicles that are environment friendly and creates less pollution. The global shift towards electric vehicles is another significant driver of silver consumption. The commodity is used in the production of EV batteries and the production of electrical contacts and switches which are essential components of electric vehicles. Electric cars depend heavily on silver. Each EV contains between 25 and 50 grams of silver, depending on the model, and hybrid cars use 18 to 34 grams of silver. Overall, the automotive sector uses 55 million ounces of silver annually, and by 2025, that amount is anticipated to increase to 90 million ounces. The demand for silver in the automotive industry, and for the creation of renewable energy, will only increase, which will inevitably drive the silver market’s growth.

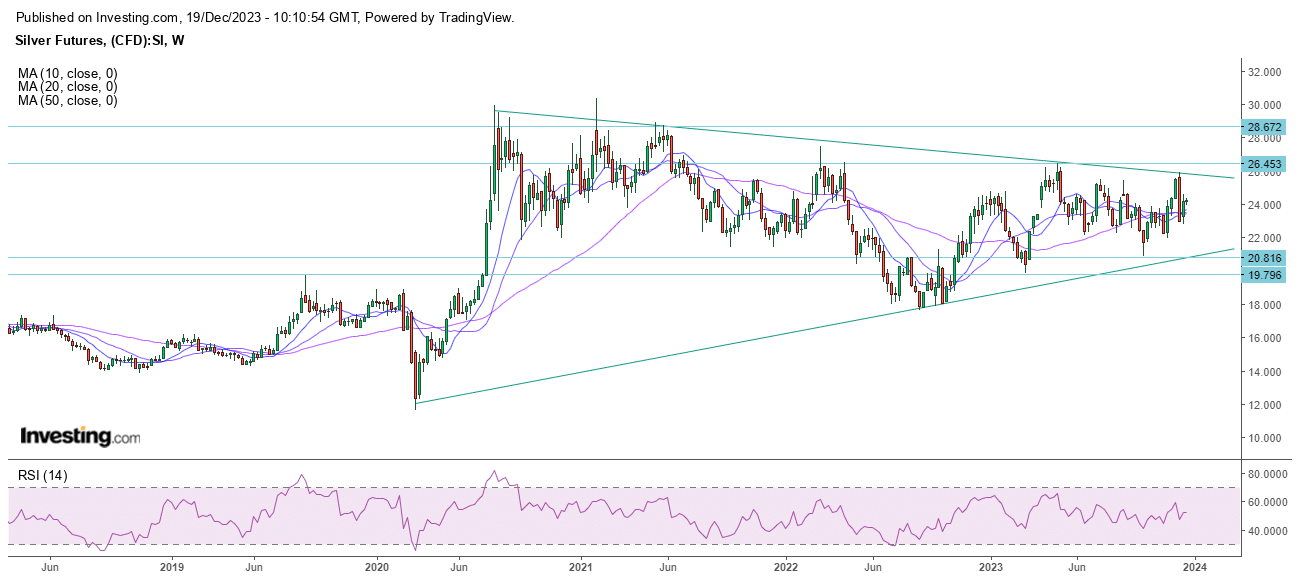

Weekly Chart of Silver (COMEX)

Analysis

COMEX Silver prices have seen volatile movement in 2023 as it moved in range of $18-26.5 range. On weekly charts prices are above 10 and 20 day and 50 day moving average. In near to medium term prices can take support near $19.80-20.80 and resistance near $26.5-28.5.

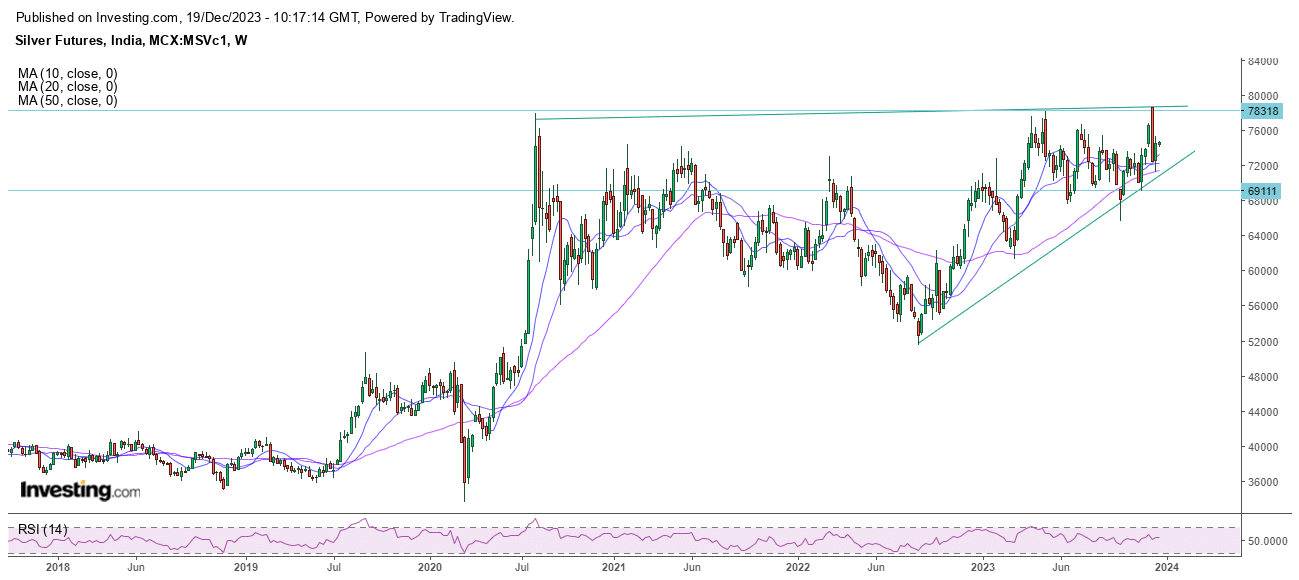

Weekly Chart of Silver (MCX)

Analysis

Silver prices in MCX have seen volatile movement in the year 2023 as it moved in wide range of 58000-78000 range. On weekly charts prices are above 10 and 20 day and 50 day moving average. Overall its prices can take support near 68000 -69000 and can face resistance near 78500-79000 in near to medium term.

Disclosure

Globe Capital Market Limited (“GCML”) is a Stock Broker registered with BSE, NSE, USE and MSEI in all the major segments viz. Capital, F & O and CDS segments. GCML is also a Depository Participant and registered with both the Depositories viz. CDSL and NSDL. Further, GCML is a SEBI registered Portfolio Manager. GCML includes subsidiaries, group and associate companies, promoters, directors, employees and affiliates.

Globe Commodities Limited, Globe Derivatives and Securities Limited & Globe Fincap Limited are subsidiaries of GCML. Rolex Finvest Private Limited, A to Z Consultants Private Limited, A to Z Venture Capital Limited, M. Agarwal Stock Brokers Private Limited, A M Share Brokers Private Limited, Shri Adinath Advertising Company Pvt. Ltd., Orient Landbase Private Limited, Bolt Synthetic Private Limited, Price ponder Private Limited and Lakshya Impex Private Limited are associates of GCML. Globe Comex International DMCC is step down subsidiary of GCML.

This report has been prepared by GCML and published in accordance with the provisions of Regulation 19 of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for general circulation or public distribution. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available to others, in any form, in whole or in part, for any purpose without prior written permission from GCML. The projections and the forecasts described in this report are based on estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections are forecasts were based may not materialize or may vary significantly from actual results and such variations will likely increase over the period of time. This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into account the particular investment objective, financial situation or needs of any individual in particular. The research analysts of GCML have adhered to the code of conduct under Regulation 24 (2) of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their own investment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particular circumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. GCML does not take any responsibility thereof.

Any such recipient shall be responsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved in securities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investors may realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.

This report has been prepared by GCML based on the information available in the public domain and other public sources believed to be reliable. Though utmost care has been taken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by GCML that such information is accurate or complete and/or is independently verified. The contents of this report represent the assumptions and projections of GCML and GCML does not guarantee the accuracy or reliability of any projection, assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable or appropriate to recipients’ specific circumstances.

Since GCML or its associates are engaged in various financial activities, they might have financial interest or beneficial ownership in various companies including subject company/companies mentioned in the report. GCML or its associates have not received any compensation for investment banking or merchant banking from the subject company in the past 12 months. GCML or its associates might have received any compensation including brokerage services and for products or services other than investment banking or merchant banking from the subject company in the past 12 months. It is confirmed that GCML or research analyst or its associates have not managed or co-managed public offering of securities for the subject company in the past 12 months.

Research analyst or GCML or its relatives’/associates’ have no material conflict of interest at the time of publication of this report. Neither research analyst nor GCML are engaged in market making activity for the subject company. It is confirmed that research analysts do not serve as an officer, director or employee of the subject company. It is also confirmed that research analyst have not received any compensation from the subject company in the past 12 months.

No material disciplinary action has been taken on GCML by any regulatory authority impacting Equity Research Analysis activities.

The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. This information is subject to change, as per applicable law, without any prior notice. GCML reserves the right to make modifications and alternations to this statement, as may be required, from time to time.

Research analyst or GCML or its relatives’/associates’ do not have actual/beneficial ownership of 1% or more in securities of the subject company, at the end of the month immediately preceding the date of publication of the document.