Natural gas prices have witnessed steep downside movement as its prices have dropped more than 65 per cent in nearly past two months amid oversupply in US and lower demand. Natural gas prices were hovering nearly $7.2 in NYMEX and nearly 600 in MCX in the last week of November 2022. Since then prices have halved and currently hovering near $2.5 in NYMEX and nearly 200 in MCX on decline in demand amid warmer weather forecasts. On the downside the price can take support near 170-180 range while upside resistance is near 270-350 in medium term.

Overview and Outlook

Natural gas prices have witnessed steep downside movement as its prices have dropped more than 65 per cent in nearly past two months amid oversupply in US and lower demand. Natural gas prices were hovering nearly $7.2 in NYMEX and nearly 600 in MCX in the last week of November 2022. Since then prices have halved and currently hovering near $2.5 in NYMEX and nearly 200 in MCX on decline in demand amid warmer weather forecasts. Much of the 2022 demand increase came from the chemical sector and the manufacturing sector. Chemical sector accounts for 29% of the total gas consumption, the largest in the industrial sector. Also, the spread between Europe and U.S. Fear of supply disruption due to Russia and Ukraine war, Supply outrages, rising coal prices rise in heating demand contributed to spurt in gas prices in first half of 2022. Europe’s gas consumption declined by more than 10% in the first eight months of 2022 compared with the same period in 2021, driven by a 15% drop in the industrial sector as factories curtailed production. The demand in China and Japan remains unchanged in that same period while contracting in India and Korea.

In near term extreme weather events can cause price spikes and volatility in natural gas prices. Freeport LNG, the second-biggest U.S. liquefied natural gas (LNG) exporter plans to restart one of three liquefaction trains at its long-idled Texas export plant .Meanwhile, investors continue to monitor the situation at the Freeport LNG export plant in Texas, which was will take until mid march for full LNG production. U.S. gas stockpiles are about 1% above the five-year (2018-2022) average for this time of year. Natural gas prices have witnessed sharp correction from recent highs on decline in demand .Meanwhile decline in rig count and powerful arctic blast which swept into the U.S. Northeast can lend support to the prices. On the downside the price can take support near 170-180 range while upside resistance is near 270-350 in medium term.

Factors affecting Natural gas prices

Production to remain tight in coming months

It is expected that the market remains tight from December to March amid weather-related issues, as the extreme weather conditions will hamper production. After the cold weather, it is expected that production will steadily increase. In 2022, production was driven by increased drilling activity in the Haynesville region in Louisiana and East Texas and in the Permian region in West Texas and Southeast New Mexico. Recent pipeline infrastructure expansions in both these regions facilitated the increases in production.

Consumption to remain variable on weather related demand

Residential and commercial natural gas consumption can be highly variable in winter months due to extreme weather events, when extreme cold weather across much of the United States led to increased residential and commercial natural gas consumption. Forecasts for colder weather in near term expected to support natural gas prices.

Europe gas storage nearly full

A late start to the 2022/23 heating season saw Europe building gas storage almost until mid-November. At a little more than 95% full, storage was essentially maxed out. This was far above the target of 80% by 1 November 2022 set by the European Commission. Ending this winter with very comfortable inventories makes the job of refilling storage over the injection season and hitting EU inventory targets of 90% by 1 November 2023 easier. Between 1 April and the end of October last year, the EU added in the region of 67 billion cubic metres (bcm) to storage. If we were to see similar storage levels at the start of the next heating season, the EU would only need to add around 43bcm of gas this year.

Decline in rig count and Arctic blast

Baker Hughes’s total rig counts showing a decline from 771 to 759 could encourage bulls to remain in command. Secondly, a powerful arctic blast swept into the U.S. Northeast pushing temperatures to perilously low levels across the region, including New Hampshire’s Mount Washington, where the wind chill dropped to 105 degrees below zero Fahrenheit.

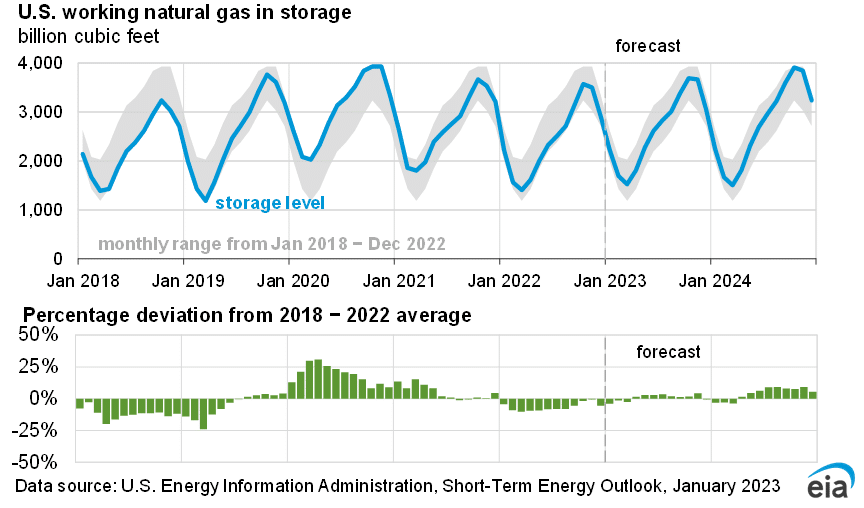

Natural gas inventory levels

Working gas in storage was 2,583 Bcf as of January 27, 2023, according to EIA estimates. This represents a net decrease of 151 Bcf from the previous week. Stocks were 222 Bcf higher than last year at this time and 163 Bcf above the five-year average of 2,420 Bcf. At 2,583 Bcf, total working gas is within the five-year historical range.

U.S. production of dry natural gas

U.S. production of dry natural gas will average about 100.0 Bcf/d from December through March, down about 0.5 Bcf/d from November due to weather-related declines, usually caused by freeze-offs and the possibility of extreme winter weather events. Mild weather in key producing regions could prevent those declines. Dry natural gas production has increased during 2022 in the United States, averaging more than 100 Bcf/d in October and November and exceeding pre-pandemic monthly production records from 2019.

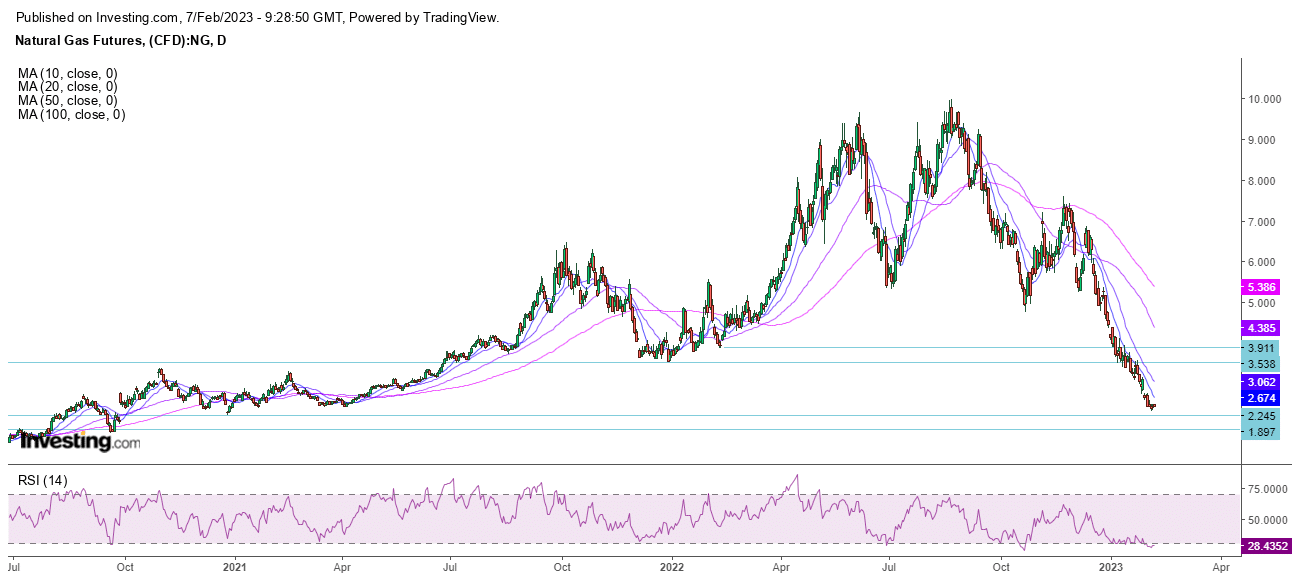

Daily Chart of Natural gas (NYMEX)

Analysis

In NYMEX Natural gas futures has been falling sharply in past two months as it fell below $2.5. On daily chart prices are hovering below the 10, 20, 50 and 100 moving averages while RSI indicator is below 30 at oversold levels. On daily chart in NYMEX the downside support lies near $2.25- 1.9 range while the upside resistance lies near $3.5 and $4.

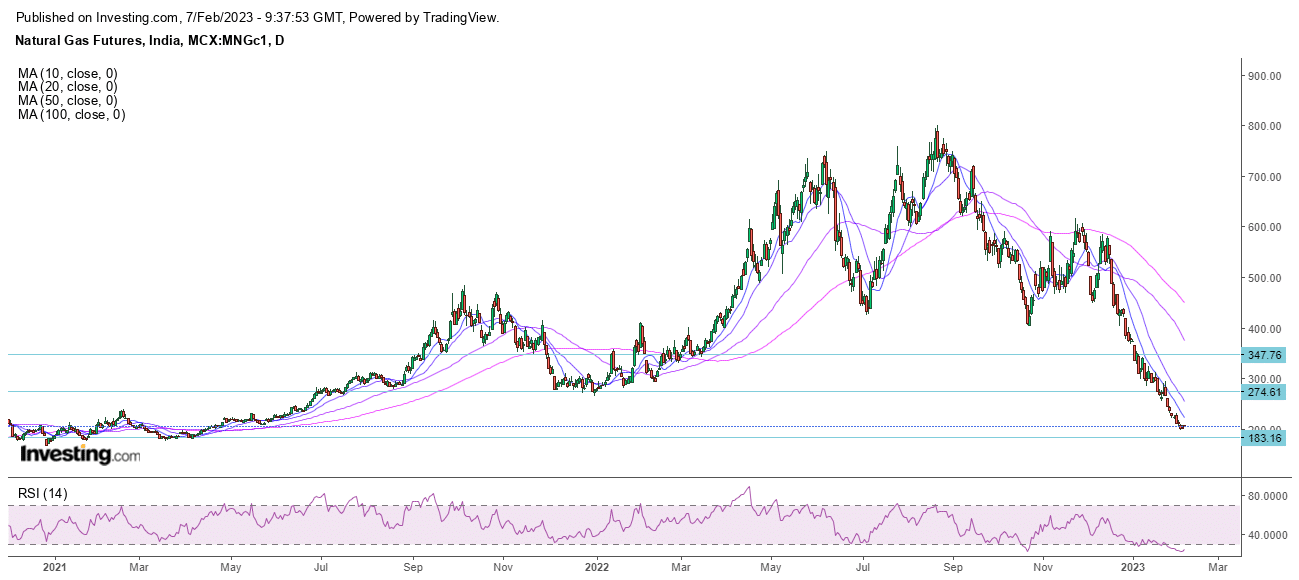

Daily Chart of Natural gas (MCX)

Analysis

In MCX sharp fall was seen in past few months in natural gas prices as they are hovering below 10, 20, 50 and 100 day moving averages and RSI below 30 at oversold levels. On the downside the price can take support near 170-180 range while upside resistance is near 270-350 in medium term.

Disclosure

Globe Capital Market Limited (“GCML”) is a Stock Broker registered with BSE, NSE, USE and MSEI in all the major segments viz. Capital, F & O and CDS segments. GCML is also a Depository Participant and registered with both the Depositories viz. CDSL and NSDL. Further, GCML is a SEBI registered Portfolio Manager. GCML includes subsidiaries, group and associate companies, promoters, directors, employees and affiliates.

Globe Commodities Limited, Globe Derivatives and Securities Limited & Globe Fincap Limited are subsidiaries of GCML. Rolex Finvest Private Limited, A to Z Consultants Private Limited, A to Z Venture Capital Limited, M. Agarwal Stock Brokers Private Limited, A M Share Brokers Private Limited, Shri Adinath Advertising Company Pvt. Ltd., Orient Landbase Private Limited, Bolt Synthetic Private Limited, Price ponder Private Limited and Lakshya Impex Private Limited are associates of GCML. Globe Comex International DMCC is step down subsidiary of GCML.

This report has been prepared by GCML and published in accordance with the provisions of Regulation 19 of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for general circulation or public distribution. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available to others, in any form, in whole or in part, for any purpose without prior written permission from GCML. The projections and the forecasts described in this report are based on estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections are forecasts were based may not materialize or may vary significantly from actual results and such variations will likely increase over the period of time. This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into account the particular investment objective, financial situation or needs of any individual in particular. The research analysts of GCML have adhered to the code of conduct under Regulation 24 (2) of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their own investment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particular circumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. GCML does not take any responsibility thereof.

Any such recipient shall be responsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved in securities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investors may realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.

This report has been prepared by GCML based on the information available in the public domain and other public sources believed to be reliable. Though utmost care has been taken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by GCML that such information is accurate or complete and/or is independently verified. The contents of this report represent the assumptions and projections of GCML and GCML does not guarantee the accuracy or reliability of any projection, assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable or appropriate to recipients’ specific circumstances.

Since GCML or its associates are engaged in various financial activities, they might have financial interest or beneficial ownership in various companies including subject company/companies mentioned in the report. GCML or its associates have not received any compensation for investment banking or merchant banking from the subject company in the past 12 months. GCML or its associates might have received any compensation including brokerage services and for products or services other than investment banking or merchant banking from the subject company in the past 12 months. It is confirmed that GCML or research analyst or its associates have not managed or co-managed public offering of securities for the subject company in the past 12 months.

Research analyst or GCML or its relatives’/associates’ have no material conflict of interest at the time of publication of this report. Neither research analyst nor GCML are engaged in market making activity for the subject company. It is confirmed that research analysts do not serve as an officer, director or employee of the subject company. It is also confirmed that research analyst have not received any compensation from the subject company in the past 12 months.

No material disciplinary action has been taken on GCML by any regulatory authority impacting Equity Research Analysis activities.

The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. This information is subject to change, as per applicable law, without any prior notice. GCML reserves the right to make modifications and alternations to this statement, as may be required, from time to time.

Research analyst or GCML or its relatives’/associates’ do not have actual/beneficial ownership of 1% or more in securities of the subject company, at the end of the month immediately preceding the date of publication of the document.