Crude oil prices witnessed downside movement in the second half of the year 2022 as it fell from high of nearly $120 to $70 that is fall of nearly 40 percent in NYMEX and from nearly 9400 in MCX to 5900 recently that is fall of nearly 37 per cent due to rising global interest rates and economic slowdown concerns. In near term oil prices will be driven by recovering demand (China reopening, aviation recovering) amid constrained supply due to low levels of investment, risks to Russia supply, the end of SPR releases, and slowdown of U.S. shale production. Prices can take support near 5800-6000 while upside resistance remain near 7600 – 7700 in MCX While in NYMEX the support is near $68-70 while resistance is near $92-94.

Overview

Crude oil prices witnessed downside movement in the second half of the year 2022 as it fell from high of nearly $120 to $70 that is fall of nearly 40 percent in NYMEX and from nearly 9400 in MCX to 5900 recently that is fall of nearly 37 per cent due to rising global interest rates and economic slowdown concerns. But the planned and unplanned oil supply disruptions in several regions can contribute to tightening fundamentals thereby supporting the prices. Recently optimism from China’s reopening and oil demand recovery outweighed concerns of a global recession. But the upside remains capped due to monetary tightening by various global central banks to curtail excess liquidity in order to curb inflation. Meanwhile geopolitical tensions between Russia Ukraine will keep prices elevated. In near term oil prices will be driven by recovering demand (China reopening, aviation recovering) amid constrained supply due to low levels of investment, risks to Russia supply, the end of SPR releases, and slowdown of U.S. shale production. Prices can take support near 5800-6000 while upside resistance remain near 7600 – 7700 in MCX While in NYMEX the support is near $68-70 while resistance is near $92-94.

Factors affecting Crude oil prices

Russia and Ukraine tensions

The Russia-Ukraine conflict has begun to have a major impact on the world energy markets. India and China have become the largest buyers of Russian oil as Western nations restrict purchases and impose sanctions. India’s imports of Russian oil have risen from a very low base at the start of the year reaching a peak in June and July, and largely maintaining these levels through to November.

EU embargo on Russian crude oil

The European Union (EU) embargo on Russian oil, which came into force on December 5, 2022, is a long-awaited sanction for Kiev that should block one of Moscow’s main sources of revenue. From December 5, 2022, it will be prohibited to unload Russian oil into an EU port. The US, UK, Japan, and Australia have made similar commitments.

G7 coalition agrees $60 per barrel price cap for Russian oil

The Group of Seven (G7) nations and Australia said they had agreed a $60 per barrel price cap on Russian seaborne crude oil. The price cap, a G7 idea, aims to reduce Russia’s income from selling oil, while preventing a spike in global oil prices after an EU embargo on Russian crude takes effect on Dec. 5. U.S. Treasury Secretary Janet Yellen said the cap will particularly benefit low- and medium-income countries that have borne the brunt of high energy and food prices. “With Russia’s economy already contracting and its budget increasingly stretched thin, the price cap will immediately cut into Putin’s most important source of revenue,” Yellen said in a statement.

OPEC failed to meet production target

In latest monthly report, OPEC revealed it had yet again failed to produce as much oil as it agreed to produce the last time it discussed output. And it wasn’t by a few thousand barrels per day, either. The shortfall was some 1.8 million barrels daily, but more importantly, that sort of undershooting of its own target has become a regular thing for the cartel.

China relaxing Covid norms will boost oil demand

In the last two weeks, China government authorities relaxed several measures that had forced many people to stay home and businesses to operate mostly remotely. The developments have been positive on energy markets, with both gas and oil prices rallying since Beijing relaxed Covid-19 norms.

Surge in US Crude oil exports

Sales of U.S. crude to other nations are now a record 3.4 million barrels per day (bpd), with exports of about 3 million bpd of refined products like gasoline and diesel fuel. Factors changing that equation this year include sanctions hurting Russia’s exports of oil and natural gas following its invasion of Ukraine, and Washington’s massive release of oil from emergency reserves to combat spiking gasoline prices U.S. government data showed net U.S. crude oil imports fell to 1.1 million barrels per day (bpd), the lowest since record keeping began in 2001. That is down sharply from five years ago, when the United States imported more than 7 million barrels per day.

OPEC+ misses production quota

The 19 OPEC+ members subject to the quota produced 310,000 bpd fewer barrels in November when compared to the month prior. But that’s still 1.81 million barrels per day short of its quota for November. OPEC’s crude production was down 770,000 bpd for November, a six-month low. The production declines were led by Saudi Arabia, which saw its output reduced by 440,000 bpd. The biggest laggards among the broader OPEC+ group now, according to Argus, are Russia, producing 670,000 bpd under target; Nigeria, producing 530,000 bpd under target, Angola, producing 350,000 bpd under target, and Malaysia, producing 170,000 under target.

EIA Inventory Data Report supporting crude oil

U.S. Energy Information Administration reported an inventory draw of 5.9 million barrels for the week to December 16. At 418.2 million barrels, U.S. crude oil inventories remain some 7 percent below the five-year average for this time of the year. The latest draw follows a weekly addition of 10.2 million barrels for the previous week—one of the biggest weekly increases in inventories this year. In gasoline, the Energy Information Administration estimated an inventory build of 2.5 million barrels for the week to December 16, which compared with a build of 4.5 million barrels for the previous week. Gasoline production averaged 9.6 million barrels daily, which compared with 9.2 million barrels daily for the previous week. In middle distillates, the EIA reported an inventory decline of 200,000 barrels for the week to December 16. This compared with a build of 1.4 million barrels for the previous week. Middle distillate production averaged 5.1 million bpd last week, which compares with 5.2 million bpd over the previous week.

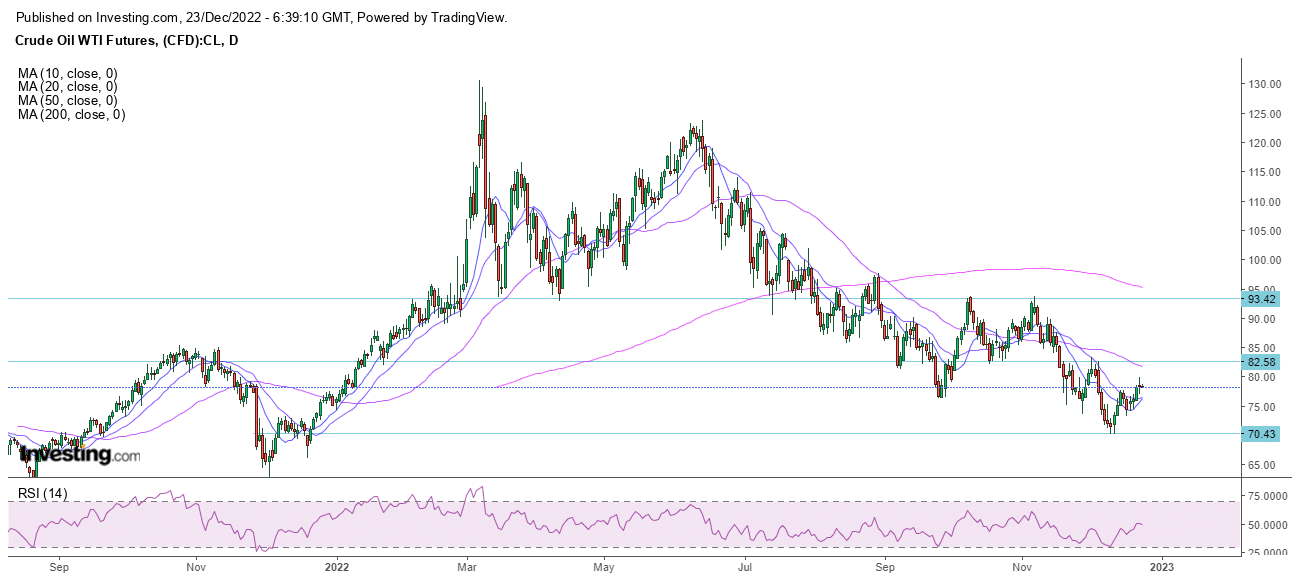

Daily Chart of Crude oil (NYMEX)

Analysis

In NYMEX some recovery can be seen in Crude oil as its prices have moved above 10 and 20 day moving averages. RSI on daily charts is 58 indicating that momentum is increasing. In near term further upside is possible towards $93-95 as downside is expected to remain capped near support level of $70.

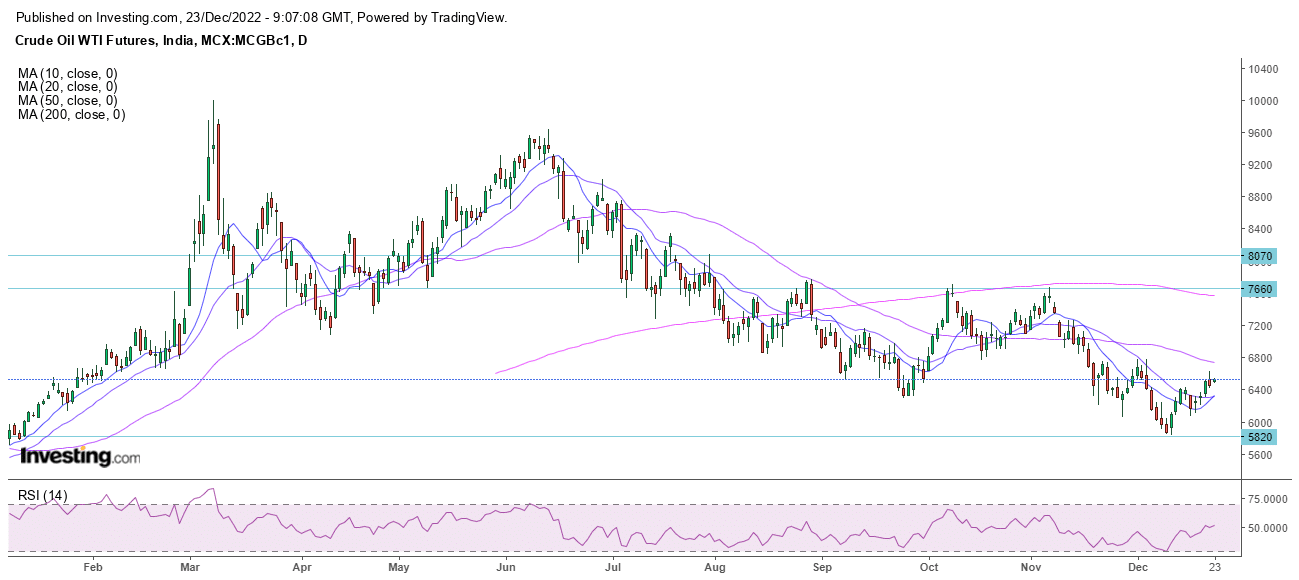

Daily Chart of Crude oil (MCX)

Analysis

In MCX some recovery is being witnessed in Crude oil as prices have been moving above the 10 and 20 day moving average. RSI indicator reading is above 50 thus indicating increase in upside momentum .In MCX the bounce back is expected to continue further as it has key support near 5800-6000 zone while upside resistance is near 7500-7600 zone.

Disclosure

Globe Capital Market Limited (“GCML”) is a Stock Broker registered with BSE, NSE, USE and MSEI in all the major segments viz. Capital, F & O and CDS segments. GCML is also a Depository Participant and registered with both the Depositories viz. CDSL and NSDL. Further, GCML is a SEBI registered Portfolio Manager. GCML includes subsidiaries, group and associate companies, promoters, directors, employees and affiliates.

Globe Commodities Limited, Globe Derivatives and Securities Limited & Globe Fincap Limited are subsidiaries of GCML. Rolex Finvest Private Limited, A to Z Consultants Private Limited, A to Z Venture Capital Limited, M. Agarwal Stock Brokers Private Limited, A M Share Brokers Private Limited, Shri Adinath Advertising Company Pvt. Ltd., Orient Landbase Private Limited, Bolt Synthetic Private Limited, Price ponder Private Limited and Lakshya Impex Private Limited are associates of GCML. Globe Comex International DMCC is step down subsidiary of GCML.

This report has been prepared by GCML and published in accordance with the provisions of Regulation 19 of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for general circulation or public distribution. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available to others, in any form, in whole or in part, for any purpose without prior written permission from GCML. The projections and the forecasts described in this report are based on estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections are forecasts were based may not materialize or may vary significantly from actual results and such variations will likely increase over the period of time. This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into account the particular investment objective, financial situation or needs of any individual in particular. The research analysts of GCML have adhered to the code of conduct under Regulation 24 (2) of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their own investment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particular circumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. GCML does not take any responsibility thereof.

Any such recipient shall be responsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved in securities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investors may realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.

This report has been prepared by GCML based on the information available in the public domain and other public sources believed to be reliable. Though utmost care has been taken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by GCML that such information is accurate or complete and/or is independently verified. The contents of this report represent the assumptions and projections of GCML and GCML does not guarantee the accuracy or reliability of any projection, assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable or appropriate to recipients’ specific circumstances.

Since GCML or its associates are engaged in various financial activities, they might have financial interest or beneficial ownership in various companies including subject company/companies mentioned in the report. GCML or its associates have not received any compensation for investment banking or merchant banking from the subject company in the past 12 months. GCML or its associates might have received any compensation including brokerage services and for products or services other than investment banking or merchant banking from the subject company in the past 12 months. It is confirmed that GCML or research analyst or its associates have not managed or co-managed public offering of securities for the subject company in the past 12 months.

Research analyst or GCML or its relatives’/associates’ have no material conflict of interest at the time of publication of this report. Neither research analyst nor GCML are engaged in market making activity for the subject company. It is confirmed that research analysts do not serve as an officer, director or employee of the subject company. It is also confirmed that research analyst have not received any compensation from the subject company in the past 12 months.

No material disciplinary action has been taken on GCML by any regulatory authority impacting Equity Research Analysis activities.

The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. This information is subject to change, as per applicable law, without any prior notice. GCML reserves the right to make modifications and alternations to this statement, as may be required, from time to time.

Research analyst or GCML or its relatives’/associates’ do not have actual/beneficial ownership of 1% or more in securities of the subject company, at the end of the month immediately preceding the date of publication of the document.