25-Jan-2024

Report on Crude oil

Crude oil prices witnessed sharp downside movement in fourth quarter of last year as prices tumbled nearly 29 per cent in NYMEX and nearly 25 percent in MCX on decline in global demand.

Crude oil prices witnessed sharp downside movement in fourth quarter of last year as prices tumbled nearly 29 per cent in NYMEX and nearly 25 percent in MCX on decline in global demand.

Overview and Outlook

Crude oil prices witnessed sharp downside movement in last two months as US gasoline inventories increased by almost 6.5MMbbls over the week- the largest increase since January 2022. This move has helped to take total US gasoline inventories back above the five-year average for this time of year. Oil prices came under pressure on expectations that OPEC+ might not deepen output cuts next year after the producer group postponed its policy meeting.

China’s decreased oil demand is playing a significant role in the global oil market, countering recent crude price surges. The country’s shift away from costly crude imports towards refined product exports and its large oil inventories are influencing global prices and supply dynamics. In near term oil prices will be driven by fears of global recession, high inflation and as well as ongoing geopolitical developments and recovery in dollar index.

The OPEC+ ministerial panel made no changes to the group’s oil output policy, and Saudi Arabia said it would continue with a voluntary cut of 1 million barrels per day (bpd) until the end of 2023, while Russia would keep a 300,000 bpd voluntary export curb until the end of December.

Moreover, the re-emergence of Iraqi Kurd barrels and new Surinamese and Guyanese barrels were also noted as factors influencing the oil market. Such developments indicate a diversified supply source, potentially adding to the volatility of prices.

In near to medium term prices are expected to take support near 5900-5800 and resistance near 7600-7700 in MCX. In NYMEX prices are expected to take support near $67-65 while facing resistance near $93 levels in NYEMX.

Factors affecting Crude oil prices

OPEC meeting

Organization of the Petroleum Exporting Countries and allies including Russia delayed a ministerial meeting at which they were expected to discuss oil output cuts to Nov. 30. Several members are reportedly unhappy about their production targets for next year, levels which were announced back in June. This is specifically the case for Angola, Congo and Nigeria, who had their production targets cut since they struggled to hit their 2023 targets. These members were unhappy back then, and it was agreed that their targets would be revisited before the end of this year and possibly revised higher.

EIA Weekly report

EIA’s weekly inventory report was fairly bearish with US crude oil inventories growing by 8.7MMbbls over the week. This leaves total US commercial crude oil inventories at a little over 448MMbbls – the highest level since July. Despite refinery utilisation remaining below average levels for this time of year (following a fairly heavy maintenance season), gasoline stocks still increased by a marginal 750Mbbls. However, the distillate market continues to tighten. Distillate fuel oil inventories fell by a little over 1MMbbls, which leaves stocks at a little under 106MMbbls- the lowest since May 2022 and at the lowest level in at least 20 years for this time of year.

U.S. rig count

The latest data from Baker Hughes shows that the US oil rig count increased by 6 over the last week to 500, which is the largest increase since February. However, the rig count is still down close to 20% YTD. The slowdown in drilling activity this year suggests that US supply growth in 2024 will be much more modest than the roughly 1MMbbls/d supply growth estimated for this year.

Russia lifted export ban on Diesel

Russia announced that it lifted its export ban on gasoline with the domestic market a lot more comfortable now. The export ban had been in place since 21 September, and it originally included diesel as well. Russia is a fairly small exporter of diesel, exporting less than 5m tonnes last year.

Weekly Chart of Crude oil (NYMEX)

Analysis

In NYMEX Crude oil prices has been witnessing consolidation at lower levels as it took support near $69-70 levels and now hovering near $75 levels. Moreover prices are bouncing from the lower bollinger band on weekly chart and can move towards middle bollinger band. In near to medium term prices are expected to take support near $69 while facing resistance near $83-85 levels.

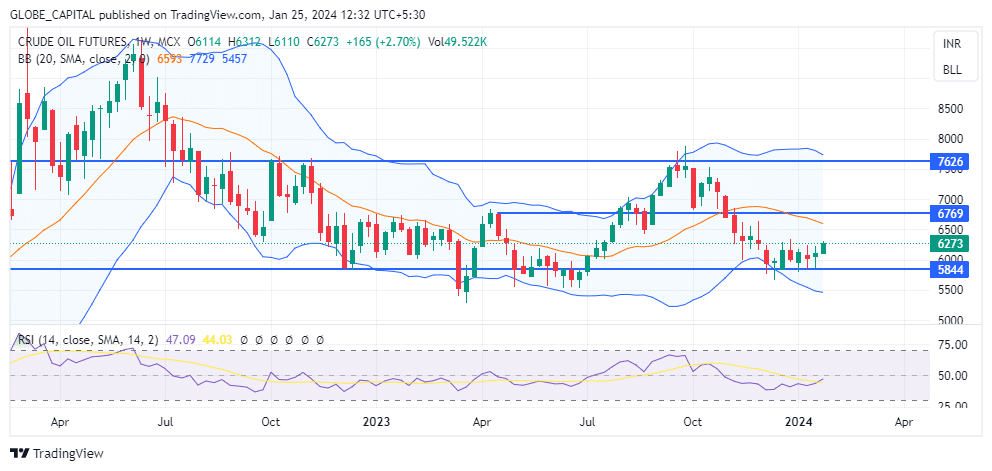

Weekly Chart of Crude oil (MCX)

Analysis

In MCX Crude oil prices have been witnessing consolidation at lower levels as it took support near 5800-5850 zone .Moreover prices are bouncing from lower bollinger band and can move towards middle bollinger band. In near to medium term prices are expected to take support near 5800-5850 levels and resistance near 6700 levels.

Disclosure

Globe Capital Market Limited (“GCML”) is a Stock Broker registered with BSE, NSE, USE and MSEI in all the major segments viz. Capital, F & O and CDS segments. GCML is also a Depository Participant and registered with both the Depositories viz. CDSL and NSDL. Further, GCML is a SEBI registered Portfolio Manager. GCML includes subsidiaries, group and associate companies, promoters, directors, employees and affiliates.

Globe Commodities Limited, Globe Derivatives and Securities Limited & Globe Fincap Limited are subsidiaries of GCML. Rolex Finvest Private Limited, A to Z Consultants Private Limited, A to Z Venture Capital Limited, M. Agarwal Stock Brokers Private Limited, A M Share Brokers Private Limited, Shri Adinath Advertising Company Pvt. Ltd., Orient Landbase Private Limited, Bolt Synthetic Private Limited, Price ponder Private Limited and Lakshya Impex Private Limited are associates of GCML. Globe Comex International DMCC is step down subsidiary of GCML.

This report has been prepared by GCML and published in accordance with the provisions of Regulation 19 of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for general circulation or public distribution. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available to others, in any form, in whole or in part, for any purpose without prior written permission from GCML. The projections and the forecasts described in this report are based on estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections are forecasts were based may not materialize or may vary significantly from actual results and such variations will likely increase over the period of time. This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into account the particular investment objective, financial situation or needs of any individual in particular. The research analysts of GCML have adhered to the code of conduct under Regulation 24 (2) of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their own investment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particular circumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. GCML does not take any responsibility thereof.

Any such recipient shall be responsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved in securities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investors may realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.

This report has been prepared by GCML based on the information available in the public domain and other public sources believed to be reliable. Though utmost care has been taken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by GCML that such information is accurate or complete and/or is independently verified. The contents of this report represent the assumptions and projections of GCML and GCML does not guarantee the accuracy or reliability of any projection, assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable or appropriate to recipients’ specific circumstances.

Since GCML or its associates are engaged in various financial activities, they might have financial interest or beneficial ownership in various companies including subject company/companies mentioned in the report. GCML or its associates have not received any compensation for investment banking or merchant banking from the subject company in the past 12 months. GCML or its associates might have received any compensation including brokerage services and for products or services other than investment banking or merchant banking from the subject company in the past 12 months. It is confirmed that GCML or research analyst or its associates have not managed or co-managed public offering of securities for the subject company in the past 12 months.

Research analyst or GCML or its relatives’/associates’ have no material conflict of interest at the time of publication of this report. Neither research analyst nor GCML are engaged in market making activity for the subject company. It is confirmed that research analysts do not serve as an officer, director or employee of the subject company. It is also confirmed that research analyst have not received any compensation from the subject company in the past 12 months.

No material disciplinary action has been taken on GCML by any regulatory authority impacting Equity Research Analysis activities.

The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. This information is subject to change, as per applicable law, without any prior notice. GCML reserves the right to make modifications and alternations to this statement, as may be required, from time to time.

Research analyst or GCML or its relatives’/associates’ do not have actual/beneficial ownership of 1% or more in securities of the subject company, at the end of the month immediately preceding the date of publication of the document.