Red metal Copper has seen roller coaster ride in 2022 as its prices went up in first quarter but fell sharply lower in remaining part of the year as stringent zero Covid norms in China and slump in factory activity in China , surging power prices in Europe and ongoing inflation in the U.S continued to exert pressure on the prices.

Overview

Red metal Copper has seen roller coaster ride in 2022 as its prices went up in first quarter but fell sharply lower in remaining part of the year as stringent zero Covid norms in China and slump in factory activity in China , surging power prices in Europe and ongoing inflation in the U.S continued to exert pressure on the prices. In MCX its prices fell nearly 25 percent from nearly 800 in June 2022 to below 600 in July 2022. Moreover concerns of a global economic slowdown due to interest rate hike by the various central banks to curb inflation kept the prices downbeat. Also the sharp bounce back in dollar index kept price under pressure.

But prices stabilized in August and September 2022 and moved in range of 625-680 in MCX. Meanwhile due to ongoing political tensions in top-producing countries such as Chile and Peru supply side was effected which capped the downside. Recently a private sector survey showed China’s factory activity contracted for the first time in three months in August while nearly 70 Chinese cities reported declines in new home prices, the most since the start of the COVID-19 pandemic. China zero Covid policy and cost pressure continued to hurt businesses, causing a slump in factory activity. Recently, China has announced billions of yuan worth of stimulus support for various sectors, including infrastructure and electric vehicles which capped the downside in red metal. Chinese copper giant Maike Metals International Ltd has been seeking help from the government and financial institutions after liquidity issues forced it to delay some payments for imported copper .In near tem stronger dollar index and monetary tightening could cap the upside in red metal but fall in inventories and supply side issues in some mine may support the prices.

Factors impacting Copper prices

Movement in Dollar index and Fed tightening measures

Dollar index is witnessing strong bullish momentum as it tested above 20 year high above 114.4 due rapid increase in rates by Federal Reserve. In recent 21 September meeting US Federal Reserve raised its target interest rate by three-quarters of a percentage point to a range of 3.00%-3.25% on Wednesday and signalled more large increases to come in new projections showing its policy rate rising to 4.40% by the end of this year before topping out at 4.60% in 2023 to battle continued strong inflation. Stronger dollar index is generally negative for copper prices.

Supply side impact of Copper mines

A group of indigenous Peruvian communities that have been blocking a key copper corridor agreed to a truce recently after the country’s prime minister said he would meet with them. Peru is the world’s No. 2 copper producer. The blockade, which lasted less than a week, affected operations by Glencore’s Antapaccay, MMG Ltd’s Las Bambas and Hudbay Minerals Inc’s Constancia. Protesters are asking the state to carry out a formal consultation process on whether Antapaccay should be allowed to build a new copper project nearby known as Coroccohuayco.

LME Copper warehouses stock positions

On-warrant base metals stocks in LME warehouses totaled 400,302 tonnes, with total stocks standing at 579,979 tonnes. This represents a 58% decrease in total stocks since the beginning of the year, when stocks stood at 1,380,100 tonnes globally.

Decline in production in Chile

According to the International Copper Study Group, production in Chile, home to the world’s largest copper mine, Escondida, was down by 6.4 percent in the first five months of 2022.Chile is the world’s largest copper producer, putting out 5.6 million MT of copper in 2021 and with reserves of 200 million MT. The value of copper exports jumped more than 40 percent in 2021, according to Chile’s central bank, with copper shipments reaching US$53.42 billion last year.

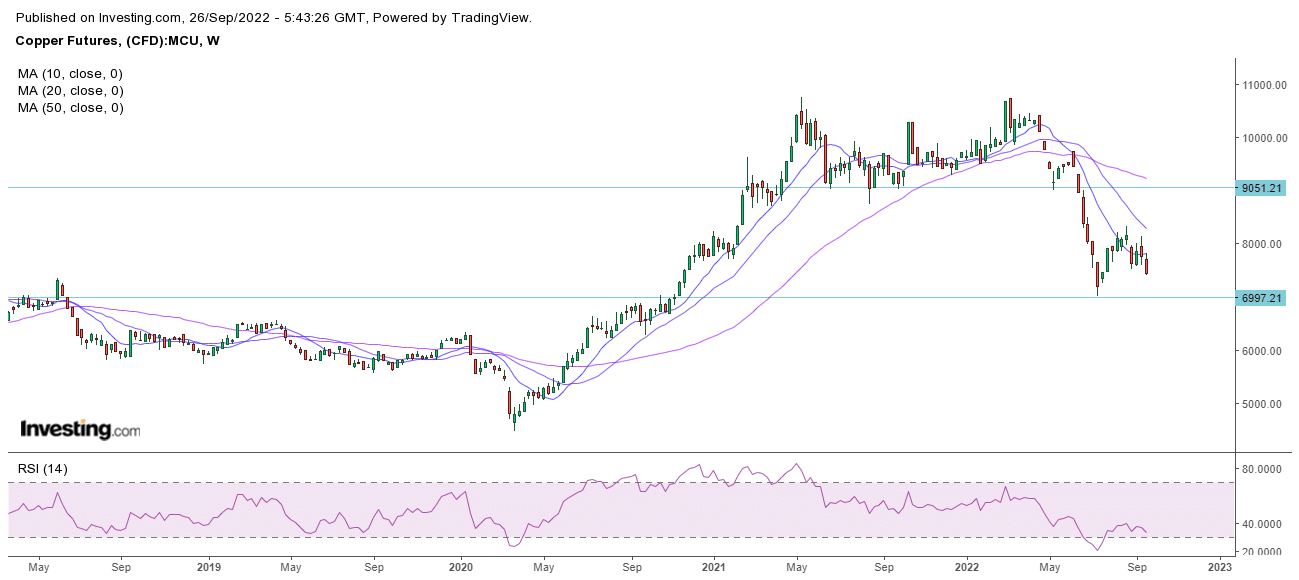

Weekly Chart of Copper (LME)

Analysis

LME Copper prices have seen steady downside movement since the April of this of the year as it faced resistance near $10400. However the prices are expected to take support near $6950-6900 zone in medium term. Prices are below 10, 20 and 50 day moving average and RSI is below 50 indicating further weakness. On weekly chart it is has key support near $6900 and resistance near $9050 in LME.

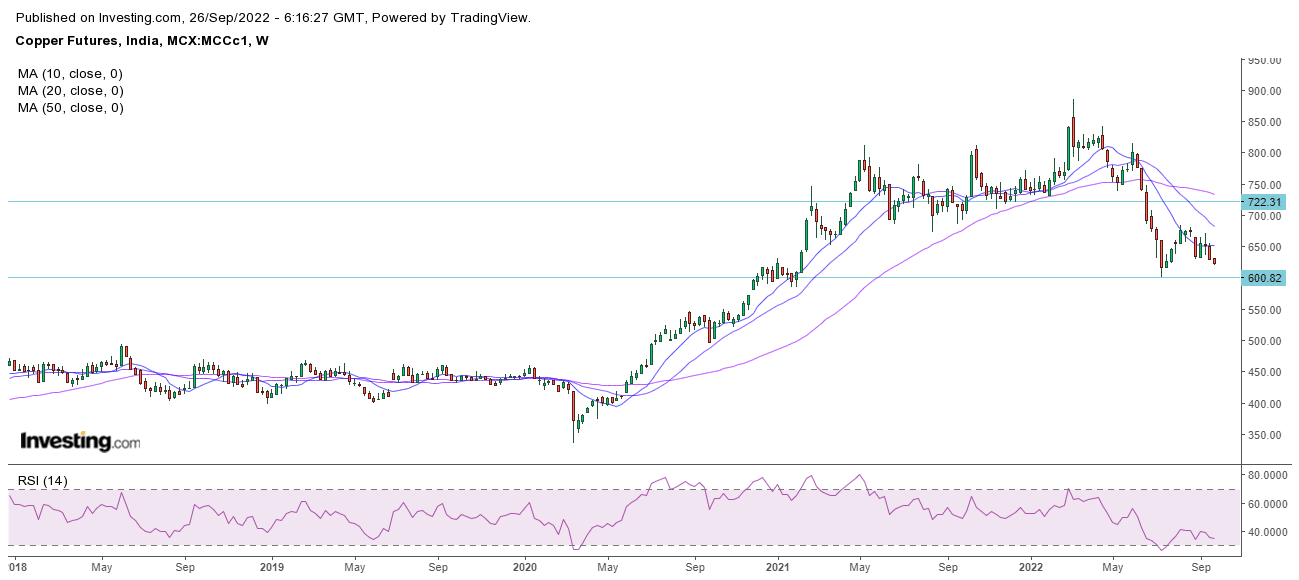

Weekly Chart of Copper (MCX)

Analysis

MCX Copper prices have shown sharp downside momentum since the April of the year as it faced resistance near 800-820 range. Prices are below 10, 20 and 50 day moving average and RSI is below 50 indicating further weakness. On weekly chart it has key support near 580-600 and resistance near 720-740 in MCX. In near to medium term further weakness can continue as it can test the support zone of 580-600 in domestic market.

Disclosure

Globe Capital Market Limited (“GCML”) is a Stock Broker registered with BSE, NSE, USE and MSEI in all the major segments viz. Capital, F & O and CDS segments. GCML is also a Depository Participant and registered with both the Depositories viz. CDSL and NSDL. Further, GCML is a SEBI registered Portfolio Manager. GCML includes subsidiaries, group and associate companies, promoters, directors, employees and affiliates.

Globe Commodities Limited, Globe Derivatives and Securities Limited & Globe Fincap Limited are subsidiaries of GCML. Rolex Finvest Private Limited, A to Z Consultants Private Limited, A to Z Venture Capital Limited, M. Agarwal Stock Brokers Private Limited, A M Share Brokers Private Limited, Shri Adinath Advertising Company Pvt. Ltd., Orient Landbase Private Limited, Bolt Synthetic Private Limited, Price ponder Private Limited and Lakshya Impex Private Limited are associates of GCML. Globe Comex International DMCC is step down subsidiary of GCML.

This report has been prepared by GCML and published in accordance with the provisions of Regulation 19 of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for general circulation or public distribution. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available to others, in any form, in whole or in part, for any purpose without prior written permission from GCML. The projections and the forecasts described in this report are based on estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections are forecasts were based may not materialize or may vary significantly from actual results and such variations will likely increase over the period of time. This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into account the particular investment objective, financial situation or needs of any individual in particular. The research analysts of GCML have adhered to the code of conduct under Regulation 24 (2) of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their own investment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particular circumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. GCML does not take any responsibility thereof.

Any such recipient shall be responsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved in securities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investors may realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.

This report has been prepared by GCML based on the information available in the public domain and other public sources believed to be reliable. Though utmost care has been taken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by GCML that such information is accurate or complete and/or is independently verified. The contents of this report represent the assumptions and projections of GCML and GCML does not guarantee the accuracy or reliability of any projection, assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable or appropriate to recipients’ specific circumstances.

Since GCML or its associates are engaged in various financial activities, they might have financial interest or beneficial ownership in various companies including subject company/companies mentioned in the report. GCML or its associates have not received any compensation for investment banking or merchant banking from the subject company in the past 12 months. GCML or its associates might have received any compensation including brokerage services and for products or services other than investment banking or merchant banking from the subject company in the past 12 months. It is confirmed that GCML or research analyst or its associates have not managed or co-managed public offering of securities for the subject company in the past 12 months.

Research analyst or GCML or its relatives’/associates’ have no material conflict of interest at the time of publication of this report. Neither research analyst nor GCML are engaged in market making activity for the subject company. It is confirmed that research analysts do not serve as an officer, director or employee of the subject company. It is also confirmed that research analyst have not received any compensation from the subject company in the past 12 months.

No material disciplinary action has been taken on GCML by any regulatory authority impacting Equity Research Analysis activities.

The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. This information is subject to change, as per applicable law, without any prior notice. GCML reserves the right to make modifications and alternations to this statement, as may be required, from time to time.

Research analyst or GCML or its relatives’/associates’ do not have actual/beneficial ownership of 1% or more in securities of the subject company, at the end of the month immediately preceding the date of publication of the document.