17-Nov-2021

Aarti Drugs Limited – Technofunda

Aarti Drugs Limited is the prime candidate to benefit from the government’s push for indigenous API manufacturing.

Aarti Drugs Limited is the prime candidate to benefit from the government’s push for indigenous API manufacturing.

Brief

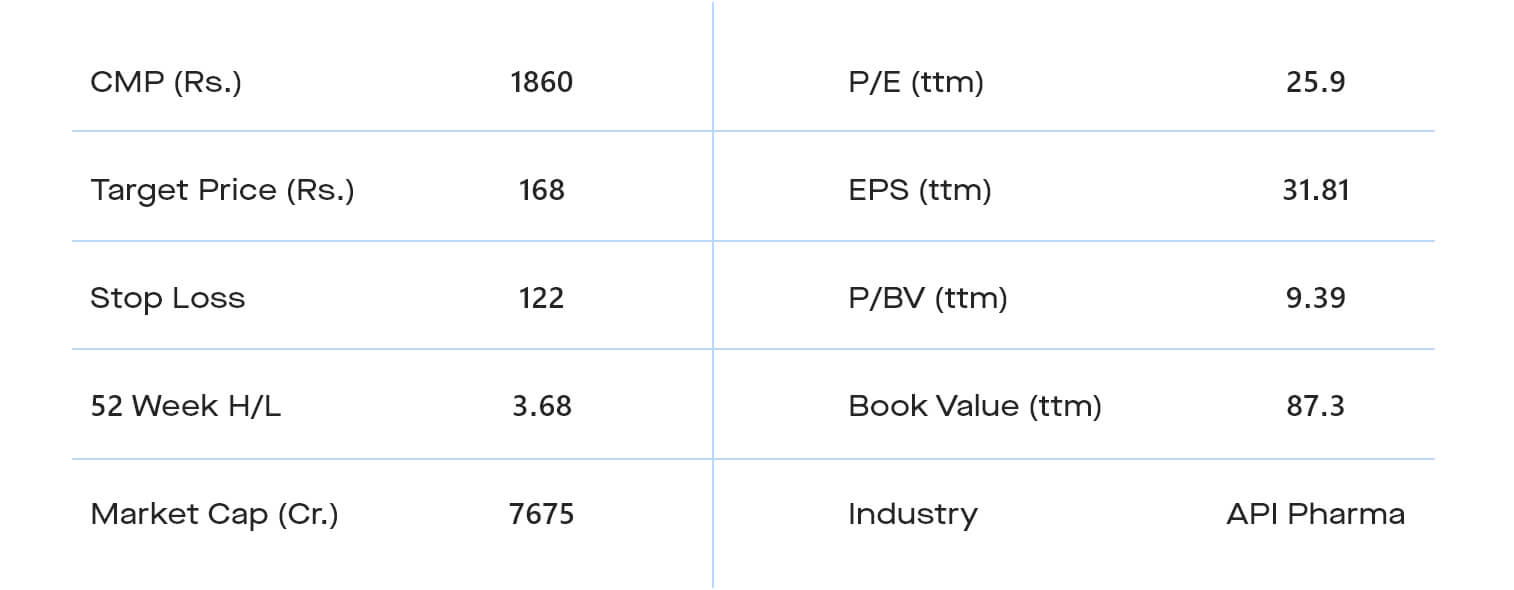

Aarti Drugs Limited is the prime candidate to benefit from the government’s push for indigenous API manufacturing. At the CMP of Rs 824, the stock is trading at ttm P/E multiple of 25.9x with ttm EPS of Rs 31.81.

Profile:

Aarti Drugs Limited was established in the year 1984 and forms part of $900 Million Aarti Group of Industries with robust R&D Division at Tarapur, Maharashtra Industrial Development Corporation (MIDC) in close vicinity to manufacturing locations. The Company is engaged in the manufacturing of Active Pharmaceutical Ingredients (APIs), Pharma Intermediates and Specialty Chemicals. and also manufactures formulations through its whollyowned subsidiary- Pinnacle Life Science Private Limited. Products under APIs includes Ciprofloxacin Hydrochloride, Metronidazole, Metformin HCL, Ketoconazole, Ofloxacin, Diclofenac derivatives etc. whereas Specialty Chemicals includes Benzene Sulphonyl Chloride, Methyl Nicotinate etc.

Key Triggers:

Minimal impact on business due to Covid-19: Healthcare Industry being into essential services has not been adversely impacted due to the countrywide lockdown. There is likely to be no impact of Covid-19 on the capital and financial resources, profitability and liquidity position of the company. The smooth movement of cash flows will ensure ability to service debt and other financing arrangements. Due to essential nature of company’s business and pharmaceuticals being included in essential goods we don’t see any impact on demand of products.

Strong Q3FY21 earnings & API business opportunities push Aarti Drugs: In the December’2020 quarter, the Company recorded consolidated quarterly revenue from operations of Rs.530.25 Crores with year-on-year increase of 11.98%. API segment contributed approximately 87% and formulation around 13% of the total consolidated revenues. Consolidated EBITDA for the quarter ended December’2020 is Rs.107.76 Crores, up by 59.11% and consolidated profit after tax for the quarter ended December’2020 is Rs.68.03 Crores, up by 144.88% on a year-on-year basis. Consolidated EBITDA margin improved from last year to 20.25%. Debt/Equity ratio of the Company reduced further down to 0.39 as of December’2020 on a consolidated basis due to strong internal accruals. This puts the Company in a good position for raising long term debt in addition to strong internal accruals to finance upcoming projects.

Valuation & View:

Aarti Drugs Limited is the prime candidate to benefit from the government’s push for indigenous API manufacturing. At the CMP of Rs 824, the stock is trading at ttm P/E multiple of 25.9x with ttm EPS of Rs 31.81.

Key Risk:

Delay in the ramp-up of the recently-added capacity; more-than-expected competition in generic APIs.

Technical View:

AARTIDRUGS has witnessed a vertical rise from 105 to 1029 levels in a short time span of 6 months. Post that, it has been trading in a congestion zone (600-810 levels) since Oct 2020. On May 10, 2021, stocks has witnessed breakout from the above mentioned congestion zone with noticeable rise in volumes.

Considering the current chart patterns, we suggest traders to buy AARTIDRUGS as we are expecting it to test 1000 levels in near term.

Summary:

Considering both the factors fundamental & technical parameter, we recommend a ‘BUY’ in AARTIDRUGS at current level for the target price of Rs. 1000 with close below stop loss of Rs. 720.

Disclosure

Globe Capital Market Limited (“GCML”) is a Stock Broker registered with BSE, NSE, USE and MSEI in all the major segments viz. Capital, F & O and CDS segments. GCML is also a Depository Participant and registered with both the Depositories viz. CDSL and NSDL. Further, GCML is a SEBI registered Portfolio Manager. GCML includes subsidiaries, group and associate companies, promoters, directors, employees and affiliates.

Globe Commodities Limited, Globe Derivatives and Securities Limited & Globe Fincap Limited are subsidiaries of GCML. Rolex Finvest Private Limited, A to Z Consultants Private Limited, A to Z Venture Capital Limited, M. Agarwal Stock Brokers Private Limited, A M Share Brokers Private Limited, Shri Adinath Advertising Company Pvt. Ltd., Orient Landbase Private Limited, Bolt Synthetic Private Limited, Price ponder Private Limited and Lakshya Impex Private Limited are associates of GCML. Globe Comex International DMCC is step down subsidiary of GCML.

This report has been prepared by GCML and published in accordance with the provisions of Regulation 19 of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for general circulation or public distribution. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available to others, in any form, in whole or in part, for any purpose without prior written permission from GCML. The projections and the forecasts described in this report are based on estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections are forecasts were based may not materialize or may vary significantly from actual results and such variations will likely increase over the period of time. This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into account the particular investment objective, financial situation or needs of any individual in particular. The research analysts of GCML have adhered to the code of conduct under Regulation 24 (2) of the Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their own investment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particular circumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. GCML does not take any responsibility thereof.

Any such recipient shall be responsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved in securities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investors may realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.

This report has been prepared by GCML based on the information available in the public domain and other public sources believed to be reliable. Though utmost care has been taken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by GCML that such information is accurate or complete and/or is independently verified. The contents of this report represent the assumptions and projections of GCML and GCML does not guarantee the accuracy or reliability of any projection, assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable or appropriate to recipients’ specific circumstances.

Since GCML or its associates are engaged in various financial activities, they might have financial interest or beneficial ownership in various companies including subject company/companies mentioned in the report. GCML or its associates have not received any compensation for investment banking or merchant banking from the subject company in the past 12 months. GCML or its associates might have received any compensation including brokerage services and for products or services other than investment banking or merchant banking from the subject company in the past 12 months. It is confirmed that GCML or research analyst or its associates have not managed or co-managed public offering of securities for the subject company in the past 12 months.

Research analyst or GCML or its relatives’/associates’ have no material conflict of interest at the time of publication of this report. Neither research analyst nor GCML are engaged in market making activity for the subject company. It is confirmed that research analysts do not serve as an officer, director or employee of the subject company. It is also confirmed that research analyst have not received any compensation from the subject company in the past 12 months.

No material disciplinary action has been taken on GCML by any regulatory authority impacting Equity Research Analysis activities.

The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. This information is subject to change, as per applicable law, without any prior notice. GCML reserves the right to make modifications and alternations to this statement, as may be required, from time to time.

Research analyst or GCML or its relatives’/associates’ do not have actual/beneficial ownership of 1% or more in securities of the subject company, at the end of the month immediately preceding the date of publication of the document.